A deep dive into Sydney’s auction clearance rates – how they are reported has got to change

July 6th, 2022

In May 2022, the RBA lifted the official cash rate for the first time since November 2010. With two further increases since then and more to come in a highly indebted residential Sydney property market, the need for reliable data is now more critical than ever.

Given that residential property is the largest Australian asset class by value, data regarding capital city auction clearance rates are as essential to the RBA as they are to property buyers and sellers.

The auction clearance rate is by far the most quoted Australian real estate statistic especially in Sydney and Melbourne and is usually regarded as a leading indicator of property prices.

Yet and as we have being saying for years, the clearance rate data published by the main research houses remain inconsistent, confusing, opaque and unreliable.

A data collecting initiative taken by an inner west Sydney agency provided us with a unique opportunity to expose just how so in a granular level snapshot. Although only a small sample, there is every reason to believe it is a representative one.

It makes for interesting reading.

As the RBA backflips from its promise that interest rates would not rise until 2024 and instead is imposing the fastest rate hikes Australia has seen, we can only hope its decision making is not influenced by published auction clearance rates.

Who are the data providers?

The main providers are Domain and the independent CoreLogic.

The third is the independent SQM Research which has recently started its own capital city series.

What are some of the many issues?

Structural

This is a room with two elephants in it.

The first is that Domain is part of a real estate portal which is also Australia’s second largest real estate marketing business. This inherent conflict of interests may help explain the massive discrepancies in Domain’s results discussed below.

The second is the RBA’s reliance on auction clearance rate data provided by private enterprise and especially, CoreLogic which, as this remark on page 35 of its August 2016 Statement on Monetary Policy confirms, has previously tripped up the RBA:

“A range of indicators suggest that conditions in the established housing market have eased this year from very strong conditions over recent years. Housing prices were little changed in the June quarter according to most published measures…In contrast, the headline CoreLogic measure of housing prices recorded very strong growth in April and May in a number of cities, to be more than 5 per cent higher over the June quarter. Recent information suggests that the strong increases reported by CoreLogic were overstated as a result of methodological changes affecting growth rates for the June quarter. The most recent data suggest that housing prices declined in most capital cities”… (emphasis ours)

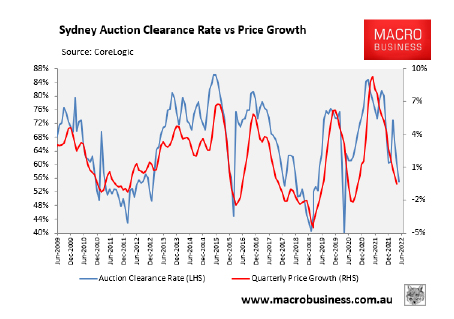

Our concern in the current and volatile environment is that 2016’s history might be repeating: while the following CoreLogic based graph suggests auction clearance rates are often a leading indicator of price growth, a closer analysis suggests otherwise during periods of heavy regulatory intervention like the present:

Between September 2016 and December 2018, APRA’s then macroeconomic measures had cooled the investor market which coincided with auction clearance rates moving from being a leading to a lagging indicator.

Not only did the same happen in 2021 Q4 and 2022 Q1, but in 2021 Q4 the relationship between auction clearance rates and price growth also inverted sharply for the first time since June 2009 and has done so again in 2022 Q1.

Hopefully, RBA’s reliance on and its relationship with, private data providers will be part of the terms of reference of the forthcoming independent review of the RBA just announced by new Treasurer, Dr Jim Chalmers.

Methodological

As this table shows, none of the three data providers follows the same methodology as the other.

Like comparing an apple with an orange and a banana, this inconsistency further confuses rather than clarifies the true picture by (and unsurprisingly), producing wildly divergent weekly Sydney auction clearance rates.

| CoreLogic (for each week) | Domain (for Saturdays only) | SQM Research (for each week) |

| Sold at + sold prior + sold after (until midnight each Sunday)/total number of reported auction results presumably including sold at + sold prior + sold after + passed in + withdrawn | Sold at + sold prior/total number of reported auction results including sold at + sold prior + sold after + passed in + withdrawn | Sold at + sold prior/total number of scheduled auctions |

Inherently unreliable data sources

All three research houses are understood to rely on data provided by selling agents whether volunteered or in response to calls from researchers.

Human nature being what it is, such information historically has flowed freely and rapidly during buoyant times but can slow to a near trickle (or worse still, be false) in less buoyant times in the property cycle.

Now is undoubtedly such a time.

With every chain only being as good as its weakest link, data gathered from volunteered hearsay is inherently unreliable as the inner west analysis below shows.

As that analysis also shows, unreported auction results are another big scourge.

The ‘preliminary auction result’ red herring

Both CoreLogic and Domain publish preliminary auction results with the promise of adjusted results later in the week.

Good luck finding them: Domain does not produce a trackable adjusted version of its Saturday auction results and CoreLogic provides neither a preliminary nor an adjusted equivalent on an individual property basis.

Commendably, SQM Research does not publish preliminary results and instead, publishes only one list of all results each Tuesday on an individual property basis for the preceding Saturday and the rest of that preceding week.

As the inner west analysis below also shows, preliminary results are a waste of time and distraction. They serve no purpose other than to get eye balls on the screens of CoreLogic and the majority Nine owned Domain.

Well regarded independent analysts including Digital Finance Analytics stopped publishing such results some time ago because of their unreliability.

Accessibility

Domain produces adjusted results for the preceding Saturday on the following Tuesday. To see what’s changed, you need to search individual properties.

Adjusted auction results on CoreLogic are accessible only by searching properties individually as a paid subscriber to the related RP Data Professional product.

Now, for the Inner West data exercise…

The Inner West agency which collected the data was Adrian William whose efforts we gratefully acknowledge.

Unlike the three research houses and other local agents, Adrian William doesn’t rely on hearsay relayed by selling agents and instead, pays for independent researchers to attend Saturday auctions in the markets they service who record the outcomes in real time.

The result of this initiative is untainted data which excludes sales prior and sales after auction.

To prepare this Newsletter, we selected the Adrian William data for Saturday 28 May 2022 as a control population of 55 inner west properties against which we monitored the results for those properties as published progressively by the three research houses from 28 May 2022 to 5 July 2022.

The Adrian William clearance rate was 27.7%.

What follows is a true and fair apples for apples comparison:

CoreLogic as at 2 June 2022 (Preliminary results)

| Unreported (A) | Wrong result (B) | % impact on reported clearance rate (A) + (B) |

| 2 | 12 | +25 |

CoreLogic as at 5 July 2022 (33 days later)

| Unreported (A) | Wrong result (B) | % impact on reported clearance rate (A) + (B) |

| 1 | 5 | +9 |

Domain as at 3 June 2022 (not updated since)

| Unreported (A) | Wrong result (B) | % impact on reported clearance rate (A) + (B) |

| 16 | 9 | +35 |

SQM Research as at 31 May 2022 (not updated since)

| Unreported (A) | Wrong result (B) | % impact on reported clearance rate (A) + (B) |

| 0 | 6 | +9 |

For some of our earlier commentary on this topic:

https://www.curtisassociates.com.au/the-missing-ingredient-in-house-price-indexes/